Investment Report February 2026: “SaaSpocalypse” and Middle East Storm

📈 Key Metrics for the Month (February 2026)

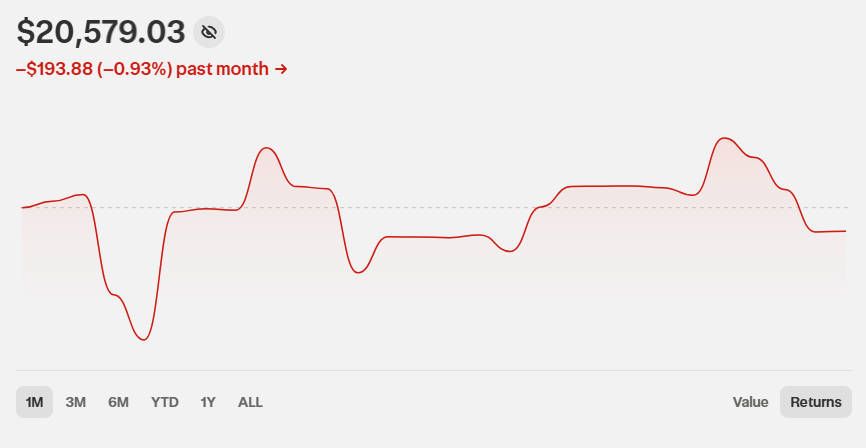

Portfolio Return: -0.93% (for the month)

Total Portfolio Value: $20,579.03 CAD

Monthly Change: -$193.88 CAD

YTD 2026 Return: +1.13%

Total Invested Since Start: $14,355 CAD (+$800 CAD added in February)

Realized Profit: +$6,224.03 CAD

ROI Since Start: +43.36%

Quick Overview

February 2026 became one of the most tense months for global markets in recent years. The portfolio finished the month with a small loss of -0.93% (-$193.88 CAD), but this is just the tip of the iceberg of events that shook financial markets.

Two global crises simultaneously:

- “SaaSpocalypse” – massive sell-off of software stocks due to fears that AI will destroy traditional SaaS companies

- US and Israeli Military Operation Against Iran – the biggest escalation in the Middle East in decades

Against the backdrop of these shocks, I:

- ✅ Added $800 CAD to TFSA

- ✅ Bought 3 new positions: XRP ETF, Amazon, QuantumScape

- 📉 Kept the portfolio from larger losses through diversification

- 💎 Received dividends of $0.81 CAD from Orla Mining

The month showed the importance of emotional resilience and a diversified portfolio. When the tech sector fell 20-30%, my positions in gold, energy, and semiconductors helped smooth the blow.

Key Events of the Month:

- 📉 “SaaSpocalypse” – software fell 20-30% on AI fears

- 💥 US and Israel attacked Iran – largest military operation in the region

- 🛢️ Oil and gas soared – Venture Global showed +36% for the month

- 🤖 Anthropic released Claude Cowork – catalyst for panic in SaaS sector

- 💰 TFSA top-up – added $800 CAD for new opportunities

- 🆕 Three new positions – XRP, Amazon, QuantumScape

🌪️ What Happened to Markets in February: Double Shock

February 2026 will be remembered as the month when two global crises hit markets simultaneously.

💻 “SaaSpocalypse”: AI Eating Software

In early February, Anthropic (the company that created Claude AI) launched Claude Cowork – a set of AI agents for automating professional workflows. Specifically, tools were introduced for:

- Legal research and analysis

- CRM and customer management

- Business analytics and reporting

- Technical documentation

Why did this cause panic?

Traditional SaaS companies (Salesforce, Workday, Atlassian, Intuit) make money on the “per-seat pricing” model. Companies pay for each employee who uses the software.

But what if AI agents can do the work of 10-20 employees? Then companies need far fewer “seats” in the software, and SaaS companies’ revenue will drop sharply.

The consequences were immediate:

- $1 trillion in capitalization wiped from the software sector in a week

- S&P Software & Services Index fell 23% YTD

- Individual companies fell 30-40% in a month:

- Workday: -10% in a day after earnings

- Atlassian: -35% in a week

- Intuit: -34% in a quarter

- Thomson Reuters: -16% in a day

Analyst reaction was divided:

✅ Optimists (JPMorgan, Goldman Sachs, Wedbush):

- “The sell-off has gone too far”

- “Entrenched companies (Microsoft, Oracle, Salesforce) have moats”

- “AI won’t replace but complement traditional software”

❌ Pessimists (Piper Sandler, Jefferies):

- “This is a structural decline, like newspapers”

- “Per-seat model is dead”

- “AI-native companies are replacing legacy SaaS”

Apt quote from Salesforce CEO Marc Benioff:

“If there is a ‘SaaSpocalypse’, it may be eaten by the ‘SaaS-quatch’ because there are a lot of companies using a lot of SaaS because it just got better with agents.”

🌍 US and Israeli Military Operation Against Iran

The second crisis hit at the end of the month – February 28, 2026.

The US and Israel launched a joint large-scale military operation against Iran with code names:

- “Roaring Lion” (Israel)

- “Operation Epic Fury” (US)

What happened:

- Strike on leadership:

- Killed Iran’s Supreme Leader Ali Khamenei

- Over 40 high-ranking Iranian commanders killed

- Military facilities destroyed across the country

- Operation objectives:

- Destruction of Iran’s nuclear program

- Elimination of missile capabilities

- Regime change

- Iranian response:

- Massive missile strikes on US bases in the Persian Gulf

- Attacks on Israel

- Threat to block the Strait of Hormuz (20% of world’s oil)

- Casualties:

- 3 US service members killed

- 5 seriously wounded

- Hundreds of Iranian military and civilians

World reaction:

- 🇨🇳 China: “Unacceptable, pushing the region into an abyss”

- 🇷🇺 Russia: “Reckless step, betrayal of diplomacy”

- 🇺🇳 UN: “Threat to international peace and security”

- 🇪🇺 EU: “Call for de-escalation”

Market impact:

- 🛢️ Oil: +8% in a day (fears of Hormuz Strait closure)

- ⛽ Gas: +12% (Venture Global shot up +36%)

- 📉 Markets: Volatility, flight to safe havens

- 🏅 Gold: New all-time high

Geopolitical context:

This isn’t the first confrontation:

- 2024: Series of direct clashes

- 2025: 12-day war with US strikes on nuclear facilities

- 2026: January – indirect negotiations in Oman failed

- 2026: February – biggest escalation in decades

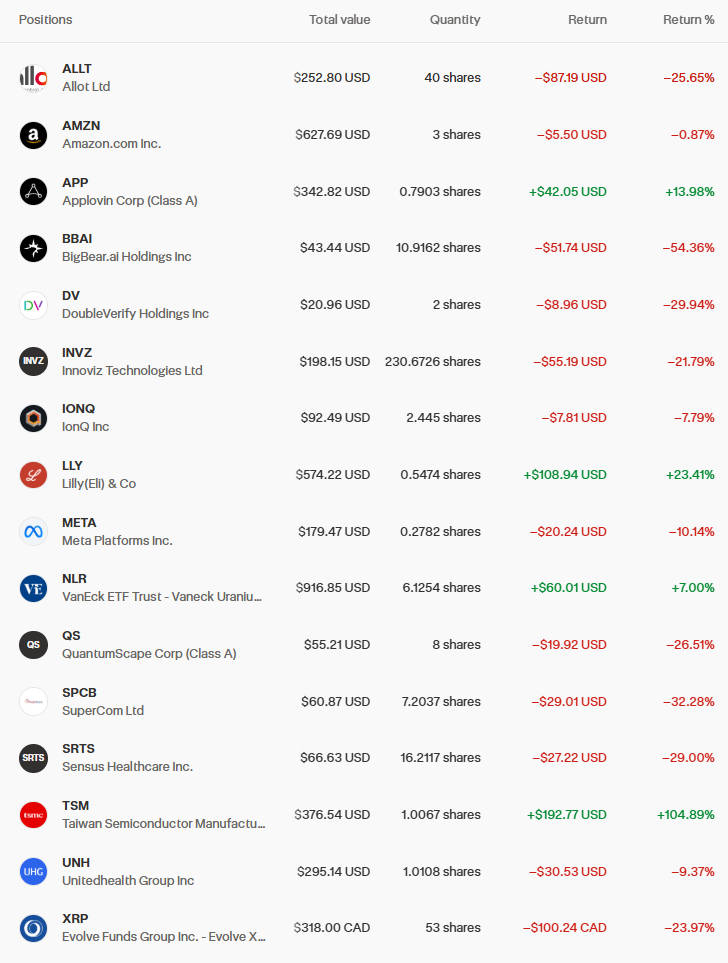

🆕 February Acquisitions: 3 Companies

In February, I added $800 CAD to TFSA and added three new positions of different natures.

1. 💰 XRP (Evolve Funds Group – Evolve XRP ETF) – 20 shares at $6.34 CAD

Total Investment: $126.80 CAD

Current Value: $318.00 CAD

Current Return: -23.97%

Portfolio Share: ~1.54% (TFSA)

Investment Thesis

XRP ETF is exposure to cryptocurrency XRP (Ripple). In February, I decided to increase this position by adding another 20 shares.

Why XRP, not Bitcoin or Ethereum?

- Legal precedent: In 2023, a court ruled that XRP is not a security in most cases. This opened doors for mass adoption.

- Real use: Ripple is used by banks for international transfers. It’s not “just speculation” but a working tool.

- Growing adoption: More and more banks and financial institutions are integrating RippleNet.

- Portfolio diversification: Adds crypto exposure without direct crypto purchase and storage.

Why through ETF?

- No need for crypto wallets

- No risk of losing keys

- Simpler taxation (within TFSA)

- Regulated investment

Strategy:

Small speculative position (1.5% of portfolio). This is a “lottery ticket” with 2-3x potential, but with understanding that I could lose everything.

Risks:

- Crypto market is extremely volatile

- Regulatory uncertainty

- Competition from Bitcoin, Ethereum, Solana

- XRP trading at -24% from my entry price

2. 📦 AMZN (Amazon) – 2 shares at $205.79 USD

Total Investment: $411.58 USD

Current Value: $627.69 USD

Current Return: -0.87%

Portfolio Share: ~3.05% (TFSA)

Investment Thesis

Amazon needs little introduction. It’s one of the “Magnificent Seven” – the world’s largest tech companies.

Why did I finally buy Amazon?

Honestly, I’ve always wanted to have Amazon in my portfolio, but the price always seemed high. In February, the stock dipped due to:

- General tech sector correction

- Fears that AI might hurt AWS (Amazon Web Services)

- Profit-taking after 2 years of rally

I decided to use this opportunity.

Three Pillars of Amazon:

- E-commerce: Dominance in online retail

- 40%+ market share in US

- Growing presence in Europe, Asia

- Amazon Prime – 200+ million subscribers

- AWS (Amazon Web Services): Cloud computing leader

- 32% of global market (more than Microsoft Azure + Google Cloud)

- Amazon’s most profitable segment (70%+ operating profit)

- AI infrastructure: companies train models on AWS

- Advertising: Third largest advertising business (after Google and Meta)

- Growth 25%+ per year

- High-margin business

Why now is a good time?

- Stock fell from peaks

- AWS continues to dominate AI infrastructure

- E-commerce remains strong

- Advertising business showing 25%+ growth

Strategy:

Long-term hold 5-10 years. Amazon is a company that will win from all megatrends:

- AI (AWS)

- E-commerce growth

- Digital advertising

Risks:

- Antitrust investigations

- Competition in AWS (Microsoft, Google)

- E-commerce growth slowdown

- High valuation (P/E ~50)

3. 🔋 QS (QuantumScape) – 8 shares at $9.39 USD

Total Investment: $75.12 USD

Current Value: $55.21 USD

Current Return: -26.51%

Portfolio Share: ~0.27% (TFSA)

Investment Thesis

QuantumScape is pure gambling. This is a company developing solid-state batteries for electric vehicles.

Why does this matter?

Traditional lithium-ion batteries have limitations:

- Slow charging (30-60 minutes)

- Limited range (~400-500 km)

- Degradation over time

- Fire risk

Solid-state batteries promise:

- ⚡ Fast charging (15 minutes to 80%)

- 🚗 Doubled range (~800-1000 km)

- 🔋 Longer lifespan

- 🛡️ Greater safety

The problem:

QuantumScape doesn’t yet produce batteries commercially. This is a pre-revenue company that:

- Burns millions of dollars on R&D

- Has a partnership with Volkswagen

- Promises mass production in 2026-2027

Why did I buy?

This is a lottery ticket with 10-20x potential if everything works out. But with understanding that there’s a high probability I’ll lose all the money.

The position is so small (0.27% of portfolio) that even if the stock goes to zero, it won’t hurt the portfolio.

Strategy:

Holding as speculation. If QuantumScape announces:

- Successful mass production

- Large contracts with automakers

- Technology breakthrough

The stock could shoot up 500-1000%. If not – I lose $75.

Risks (very high):

- Company may not achieve commercial production

- Competition from Toyota, Samsung, others

- Technology may not work at scale

- Cashburn – company loses money quarterly

- Stock already fell -26% from my entry price

Honest conclusion:

This is gambling, not investing. But with such a small position – why not? 🎲

🏆 Top Positions of the Month

🟢 Best Performers of February

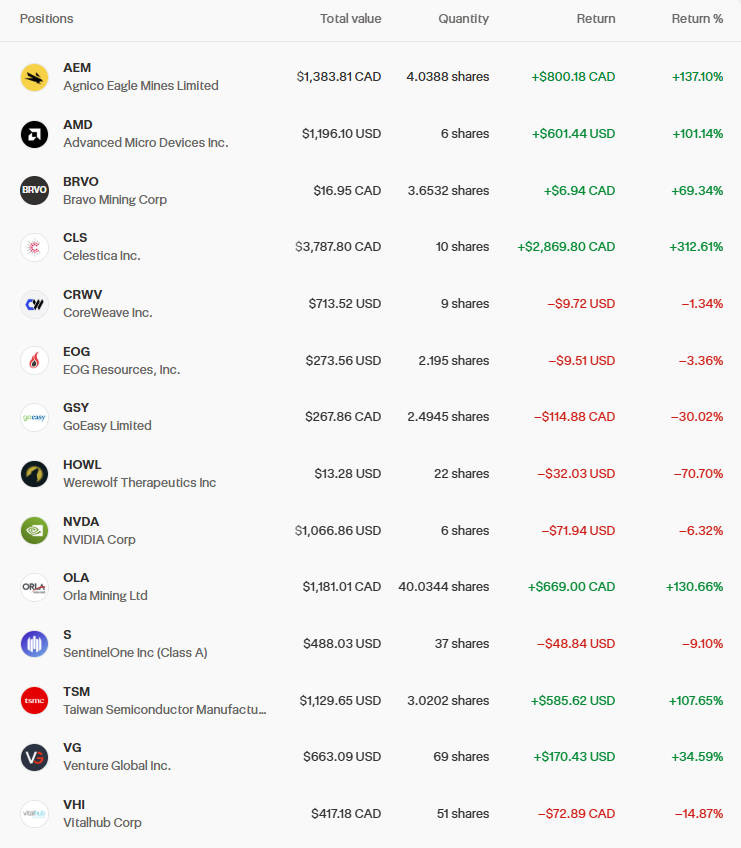

1. AEM (Agnico Eagle Mines) – +137.10% 🏆

Current Value: $1,383.81 CAD

Return: +137.10%

Portfolio Share: 6.72% (RRSP)

Comment:

Agnico Eagle continues to win from high gold prices. February’s geopolitical shocks (operation against Iran) pushed gold to new all-time highs, and gold mining companies surged along.

Gold is trading at $2,150+ per ounce (all-time high), meaning record profits for AEM.

What’s next:

Holding. Gold remains a safe haven asset in times of geopolitical instability. While wars and uncertainty continue – gold will rise.

2. AMD (Advanced Micro Devices) – +101.14% 🥈

Current Value: $1,196.10 USD

Return: +101.14%

Portfolio Share: 5.81% (RRSP)

Comment:

AMD pulled back slightly from +138% (January) to +101% (February) due to general semiconductor sector correction. But the company remains one of the strongest positions.

Latest news:

- AMD MI300X GPUs continue to show strong demand

- Microsoft and Meta use AMD for NVIDIA diversification

- Data center segment growth continues

What’s next:

Long-term hold. AMD is one of three players in AI chips (along with NVIDIA and Intel), and it continues to take market share.

3. TSM (Taiwan Semiconductor) – +107.65% (RRSP) / +104.89% (TFSA) 🥉

RRSP: $1,129.65 USD (+107.65%)

TFSA: $376.54 USD (+104.89%)

Portfolio Share: 7.31% (total)

Comment:

TSMC showed fantastic recovery from +83% (January) to +107% (February)! The company benefited from:

- Strong demand for AI chips (NVIDIA, AMD, Apple)

- Successful 3nm process launch

- Announcement of new orders from Apple for A18 chips

TSMC remains irreplaceable in the world of semiconductors. No other company can produce chips at this level.

What’s next:

One of the highest quality positions. Holding, possible additions on dips.

4. VG (Venture Global) – +34.59%

Current Value: $663.09 USD

Return: +34.59%

Portfolio Share: 3.22% (RRSP)

Comment:

Venture Global remains one of the best January acquisitions! Military operation against Iran raised gas and oil prices, and VG shot up.

Threats of Hormuz Strait closure (through which 20% of world oil passes) led to panic in energy markets, and LNG companies got a huge boost.

What’s next:

Holding. Energy security is a decades-long trend, and Venture Global remains one of the beneficiaries.

5. OLA (Orla Mining) – +130.66% 💎

Current Value: $1,181.01 CAD

Return: +130.66%

Dividends Received: $0.81 CAD

Comment:

Second gold mining company in the portfolio that benefited from rising gold prices. OLA also paid small dividends ($0.81 CAD).

Orla Mining is a young company with strong potential. It develops deposits in Mexico and the US.

What’s next:

Holding. Gold remains strong, and OLA has potential for further growth.

🔴 Biggest Losses of February

1. HOWL (Werewolf Therapeutics) – -70.70% 💔

Current Value: $13.28 USD

Return: -70.70%

Portfolio Share: 0.06% (TFSA)

Comment:

The worst investment in the portfolio continues to fall. Biotech remains the riskiest sector, and HOWL is a bright example.

But the position is so small (0.06%) that it doesn’t matter.

What’s next:

Holding as a reminder of biotech risks. If the company announces a breakthrough – might recover. If not – will lose another $13.

2. BBAI (BigBear.ai) – -54.36%

Current Value: $43.44 USD

Return: -54.36%

Portfolio Share: 0.21% (TFSA)

Comment:

Second worst position. AI hype didn’t help BigBear.ai, and the company continues to fall.

What’s next:

Holding as speculation, but chances of recovery are decreasing.

3. GSY (GoEasy) – -30.02%

Current Value: $267.86 CAD

Return: -30.02%

Portfolio Share: 1.30% (RRSP)

Comment:

GoEasy suffered from general financial sector correction. The company provides consumer loans, and in conditions of high Fed interest rates, business is under pressure.

4. SPCB (SuperCom) – -32.28%

Current Value: $60.87 USD

Return: -32.28%

Portfolio Share: 0.30% (TFSA)

Comment:

SuperCom is a microcap company engaged in electronic monitoring (GPS bracelets for prisoners). High volatility -32% per month is normal for such small companies.

5. ALLT (Allot) – -25.65%

Current Value: $252.80 USD

Return: -25.65%

Portfolio Share: 1.23% (TFSA)

Comment:

Allot (cybersecurity) suffered from general tech sector sell-off. The company has a strong product, but the market is devaluing all small-cap tech.

🎯 Analysis of Key Positions

1. Celestica (CLS) – Champion Under Pressure

January: +316.81%

February: +312.61%

Change: -4.20% for the month

Current Value: $3,787.80 CAD

Portfolio Share: 18.40% (RRSP)

What happened:

Celestica continued declining from peak +423% (November) → +342% (December) → +316% (January) → +312% (February).

In 3 months, the stock lost -26% from peak, although it remains at +312% from entry price.

Reasons for decline:

- General tech sector correction (SaaSpocalypse hit everyone)

- Profit-taking by investors after 2 years of rally

- Concerns about capital expenditure cycle on data centers

Has anything fundamentally changed?

NO. Celestica continues to:

- Manufacture equipment for Microsoft, Google, Meta data centers

- Show 20%+ annual revenue growth

- Benefit from AI boom (data center needs growing)

My decision:

Holding entire position. This is the portfolio’s biggest bet (18.4%), and I understand the risk. But I believe the company’s quality hasn’t changed, and the stock can return to peaks.

Alternative scenarios:

- ✅ Bullish: Stock returns to $450-500 CAD (+40-50% from current price)

- 📊 Base: Stock consolidates at $350-400 CAD

- ❌ Bearish: Stock falls to $250-300 CAD (-30-40%)

I’m betting on bullish or base scenario.

2. NVIDIA (NVDA) – Volatility of AI King

January: +0.24%

February: -6.32%

Change: -6.56% for the month

Current Value: $1,066.86 USD

Portfolio Share: 5.18% (RRSP)

What happened:

NVIDIA fell from $189.80 (January entry price) to $177.81 (end of February). This is a decline of -6.32%, which is better than the overall tech sector (-20-30%).

Reasons for decline:

- “SaaSpocalypse” – fears that AI isn’t paying off as quickly as expected

- ROI concerns – companies investing hundreds of billions in AI, but profits not yet visible

- Profit-taking after 2 years of 500%+ growth

Has anything fundamentally changed?

NO. NVIDIA remains:

- Absolute monopolist in AI chips (80%+ market)

- Demand for H100/H200/Blackwell GPUs remains huge

- Queue for new chips – months of waiting

- Every AI company depends on NVIDIA

My decision:

Holding and ready to add on further dips. If stock falls to $150-160, will add 2-3 more shares.

Long-term thesis unchanged:

AI isn’t hype. It’s a fundamental economic change, and NVIDIA powers this revolution.

3. CoreWeave (CRVW) – “Gold Rush Shovels” Under Pressure

January: +15.20%

February: -1.34%

Change: -16.54% for the month

Current Value: $713.52 USD

Portfolio Share: 3.47% (RRSP)

What happened:

CoreWeave fell from peak +15% to -1.34%. This is a sharp decline of -16.54% in a month.

Reasons for decline:

Same “SaaSpocalypse” fears:

- What if demand for AI infrastructure isn’t that big?

- What if companies cut AI spending?

- What if hyperscalers (AWS, Azure, Google Cloud) crush CoreWeave?

Has anything fundamentally changed?

NO. CoreWeave continues to:

- Sign long-term contracts with AI companies

- Expand capacity

- Show revenue growth

My decision:

Holding. CoreWeave is a young public company (IPO 2024), and high volatility is normal. Long-term thesis hasn’t changed.

4. SentinelOne (S) – Cybersecurity Under Fire

January: -3.67%

February: -9.10%

Change: -5.43% for the month

Current Value: $488.03 USD

Portfolio Share: 2.37% (RRSP)

What happened:

SentinelOne continued declining from -3.67% to -9.10%. Cybersecurity companies suffered from general tech sector sell-off.

Reasons for decline:

- “SaaSpocalypse” hit all SaaS companies

- SentinelOne is still unprofitable (though revenue growing 30%+ annually)

- Competition with CrowdStrike (market leader)

Has anything fundamentally changed?

NO. Cybersecurity remains critical for every company. Cyber threats aren’t disappearing – they’re only growing.

My decision:

Holding. SentinelOne is a long-term bet for 3-5 years. Short-term volatility doesn’t change the thesis.

📊 Portfolio Structure

Sector Allocation (February 2026):

- Technology / AI / Semiconductors: ~35%

- AMD, TSM, NVIDIA, CoreWeave, META, AMZN

- Gold and Resources: ~15%

- AEM, OLA, BRVO

- Energy / LNG: ~8%

- VG, NLR, EOG

- Cybersecurity: ~5%

- SentinelOne, ALLT

- Financials: ~3%

- GSY

- Biotech: ~0.5%

- HOWL, SRTS

- Other (small positions): ~8%

- LLY, APP, UNH, SPCB, DV, INVZ, BBAI, IONQ, QS, XRP

- Cash: ~0%

Diversification Analysis:

Portfolio is well-diversified across sectors:

- ✅ Tech/AI – main bet, but not the only one

- ✅ Gold – safe haven in crisis

- ✅ Energy – benefited from geopolitics

- ✅ Cybersecurity – long-term trend

Problem Areas:

- ❌ Too many small, illiquid positions (HOWL, BBAI, SPCB, QS)

- ❌ Some positions <1% of portfolio – too small to matter

Largest Positions (Top 10):

- CLS (Celestica): 18.40%

- AEM (Agnico Eagle): 6.72%

- TSM (Taiwan Semi): 7.31% (RRSP + TFSA)

- AMD: 5.81%

- OLA (Orla Mining): 5.74%

- NVDA (NVIDIA): 5.18%

- CRVW (CoreWeave): 3.47%

- AMZN (Amazon): 3.05%

- VG (Venture Global): 3.22%

- S (SentinelOne): 2.37%

Total Top 10: ~61% of portfolio

Concentration:

Portfolio is quite concentrated – top 10 positions account for 61%. This is a conscious choice: quality > quantity.

💡 February Lessons

What Worked ✅

1. Diversification Saved the Portfolio

When the tech sector fell 20-30%, my positions in gold (+137%, +130%) and energy (+34%) helped smooth the blow.

Result: -0.93% instead of potential -10-15%.

Lesson: Don’t keep all eggs in one basket, even if that basket is called “AI”.

2. Emotional Resilience During Panic

February showed the worst days for tech sector in years. “SaaSpocalypse” created panic, and many investors sold at the worst point.

I didn’t sell anything. On the contrary, I:

- Added $800 to account

- Bought Amazon on dip

- Added XRP and QS as speculations

Lesson: Best opportunities appear during panic.

3. Gold as Safe Haven Works

AEM (+137%) and OLA (+130%) showed that gold isn’t just an “old-fashioned” asset. It’s insurance against geopolitical crises.

When US and Israel attacked Iran, gold hit an all-time high.

Lesson: Always keep 10-15% of portfolio in assets that don’t correlate with tech/stocks.

What Can Be Improved 📚

1. Too Many Dead Weight Positions

HOWL (-70%), BBAI (-54%), SPCB (-32%), ALLT (-25%) – these are ballast of the portfolio.

These positions occupy ~$500 USD of capital that could work better in NVIDIA, Amazon, or even gold.

Plan: Sell in March-April when there’s any recovery.

2. XRP and QS – Too Early to Judge

XRP (-24%) and QS (-26%) are both in the red. These are speculative positions, and they need time.

But if in 3-6 months they remain at -30-40%, need to admit mistake and exit.

Lesson: Lottery tickets may not work out. Need to have stop-loss in mind.

3. CoreWeave and SentinelOne – Patience

Both positions are in the red after first month:

- CoreWeave: -1.34%

- SentinelOne: -9.10%

But these are long-term bets for 3-5 years. One month means nothing.

Plan: Hold and ignore short-term fluctuations.

🔮 What’s Ahead for Markets?

Macroeconomic Factors

1. Will “SaaSpocalypse” Continue?

Analysts are divided:

✅ Optimistic scenario:

- Sell-off has gone too far

- AI will complement SaaS, not replace it

- Entrenched companies (Microsoft, Salesforce) will adapt

❌ Pessimistic scenario:

- This is structural decline (like newspapers in 2000s)

- Per-seat model is dead

- AI-native companies replacing legacy SaaS

My opinion: Truth is in the middle. Some SaaS companies (with strong moats) will adapt. Others (weak, with easily replaceable products) will disappear.

2. Consequences of Military Operation Against Iran

This is the biggest unknown. Possible scenarios:

✅ Short-term escalation:

- Iran responds, but limitedly

- Conflict stabilizes in 1-2 months

- Oil/gas prices slightly decrease

❌ Long-term war:

- Hormuz Strait blockade

- Global energy crisis

- Recession due to high energy prices

3. Fed and Interest Rates

Fed keeps rates at 5.25-5.50%. Inflation remains high (~3-4%).

This means:

- High rates = pressure on tech stocks

- Growth may slow

- Consumer under pressure

Technology Trends

1. AI Continues to Grow

Despite “SaaSpocalypse”, AI revolution won’t stop:

- NVIDIA will continue selling GPUs

- AWS/Azure/Google Cloud will continue building data centers

- New AI applications will emerge

2. Semiconductors Remain Critical

Chips are the oil of the 21st century. Every trend (AI, EV, IoT, 5G) needs semiconductors.

AMD, TSM, NVIDIA will remain winners.

3. Cybersecurity Doesn’t Disappear

On the contrary, with AI, cyber threats only grow. SentinelOne and similar companies have a long-term future.

📝 Plans for March 2026

1. Monitoring and Patience

March is a month of observation, not active actions.

What to track:

- 📊 Earnings season: NVIDIA, AMD, Amazon, CoreWeave will report for Q4 2025 / Q1 2026

- 🌍 Geopolitics: Development of situation with Iran

- 💻 “SaaSpocalypse”: Will software sector stabilize?

2. Possible Sales of Weak Positions

If there’s any recovery:

- ❌ HOWL (-70%): Sell and realize loss

- ❌ BBAI (-54%): Sell if no news

- ❌ SPCB (-32%): Consider selling

Freed capital (~$500-600 USD) to reinvest in:

- NVIDIA (on dips)

- Amazon (add 1 share)

- TSM (add on dips)

3. Adding to NVIDIA When Possible

If NVIDIA falls to $150-160, will add 2-3 more shares.

Long-term thesis unchanged, and every dip is an opportunity.

4. Continue Portfolio Cleanup

Goal: reduce from 28-29 to 20-22 positions.

Sell the weakest, concentrate on quality.

5. Monitor XRP and QS

These two positions are lottery tickets. Give them 3-6 months to recover.

If in six months they remain at -30-40%, admit mistake and exit.

🎯 February Conclusions

February 2026 became a stress test for the portfolio. Two global crises simultaneously:

- “SaaSpocalypse” in tech sector

- Military operation against Iran

Result: -0.93% – not bad given the circumstances.

Key Conclusions:

- Diversification Saves

Gold (+137%, +130%) and energy (+34%) compensated tech decline. - Emotional Resilience More Important Than Analysis

Panic creates opportunities, not threats. - Quality Companies Survive Crises

AMD, TSM, NVIDIA, Celestica – all fell, but fundamentals haven’t changed. - Lottery Tickets Are Gambling

XRP and QS can shoot up, or can fall to zero. Must be ready for both scenarios. - Markets Are Unpredictable

No one could predict “SaaSpocalypse” or war with Iran. Therefore, must be ready for anything.

Ahead – March.

We’ll watch earnings, track geopolitics, and prepare for new opportunities.

Markets are volatile, but long-term thesis unchanged:

Technology, AI, semiconductors, gold, energy – these are megatrends of the next 10 years.

And I’m staying in the game. 💪🚀

📌 Key Portfolio Metrics

| Metric | Value |

|---|---|

| Total Value | $20,579.03 CAD |

| Monthly Return | -0.93% |

| YTD 2026 | +1.13% |

| ROI Since Start | +43.36% |

| Invested | $14,355 CAD |

| Profit | +$6,224.03 CAD |

| Number of Positions | 28 |

| Dividends Received | $0.81 CAD |

Next Report: March 2026 📊

See you in a month! 👋